Real-Time Payments at Scale

What Instant Payments Actually Demand

Instant payments have quietly crossed the line from launch to infrastructure. Most of the country can reach a real-time rail now, which was not true a couple of years ago. But from where I sit, having spent a chunk of my career in payments, the milestone is not the interesting part. The interesting part is the gap between being connected to a rail and actually running meaningful volume across it, and the operational weight that real-time quietly piles onto a bank.

Connected Is Not the Same as Using

Adoption headlines focus on how many institutions have joined a rail, and by that measure real-time payments have spread fast. But joining is the easy part. Actual volume on the instant rails is still a rounding error next to ACH, which keeps moving the overwhelming majority of payments the way it has for decades.

That gap does not surprise me. Being reachable on a network and building real-time into the products and habits of clients and staff are two different projects. The first is a connection. The second is a change in how money actually moves through the institution, and that takes much longer.

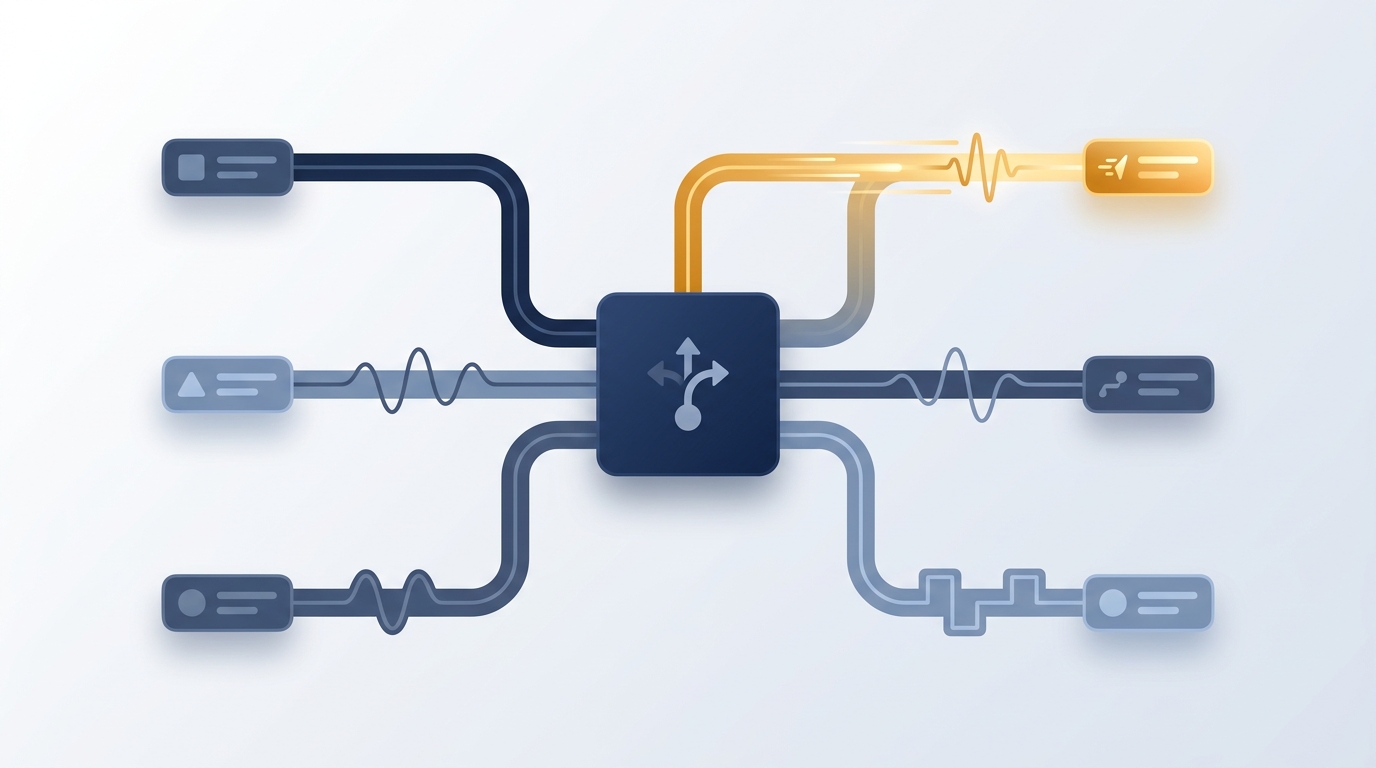

The Real Problem Is Many Rails

Here is the part that gets underestimated. The challenge was never adding one new rail. It is that a bank now runs several at once, ACH, wires, the card networks, and two separate instant rails, each with its own speed, cost, cutoff times, and risk profile. Every one of them has to be reconciled, monitored, and supported.

The clean way to handle that is a payment hub, a single internal layer that the rest of the bank talks to, with the individual rails sitting behind it. Route a payment to the hub and let it decide which rail fits. The messy way, which is unfortunately common, is bolting each new rail directly onto a legacy core one integration at a time, until you have a tangle nobody fully understands. I will take the hub every time.

Real-Time Breaks Batch Assumptions

The deeper challenge is that instant payments violate assumptions baked into how banks were built. Batch systems assume time. A window to check a payment, reconcile accounts overnight, and catch a mistake before it settles. They assume a quiet period when the system can close to run the nightly work.

Real-time erases all of that. A payment clears in seconds, at any hour, and it does not come back. Fraud has no cooling-off window. Liquidity has to be watched around the clock instead of squared up once a day. The systems can never go dark for the nightly batch, because there is no night anymore. Bolting that reality onto infrastructure designed for batch is the actual engineering problem, and it is harder than connecting to the rail ever was.

What It Takes

Instant payments are infrastructure reality now, even if they are not yet a client expectation. That expectation is coming, the same way it came for everything else that started as a novelty and became the default. The banks that will be ready are the ones treating their rails as a portfolio behind a hub, and taking the always-on, irreversible nature of real-time seriously instead of treating it as ACH that happens to be faster. It is not. It is a different way for money to move, and it asks for a different way to operate.